The changes in the semiconductor industry are accelerating, and advanced packaging is no longer just an afterthought. Renowned analyst Lu Xingzhi stated that if advanced processes are the power center of the silicon era, then advanced packaging is becoming the frontier fortress of the next technological empire.

In a post on Facebook, Lu pointed out that ten years ago, this path was misunderstood and even overlooked. However, today, it has quietly transformed from a "non-mainstream Plan B" into a "mainstream track Plan A."

The emergence of advanced packaging as the frontier fortress of the next technological empire is not coincidental; it is the inevitable result of three driving forces.

The first driving force is the explosive growth in computing power, but the progress in processes has slowed. Chips must be cut, stacked, and reconfigured. Lu stated that just because you can achieve 5nm does not mean you can fit in 20 times the computing power. The limits of photomasks restrict the area of chips, and only Chiplets can bypass this barrier, as seen with Nvidia's Blackwell.

The second driving force is the diverse applications; chips are no longer one-size-fits-all. System design is moving towards modularization. Lu noted that the era of a single chip handling all applications is over. AI training, autonomous decision-making, edge computing, AR devices—each application requires different combinations of silicon. Advanced packaging combined with Chiplets offers a balanced solution for design flexibility and efficiency.

The third driving force is the soaring cost of data transport, with energy consumption becoming the primary bottleneck. In AI chips, the energy consumed for data transfer often exceeds that of computation. The distance in traditional packaging has become a stumbling block for performance. Advanced packaging rewrites this logic: bringing data closer makes it possible to go further.

Advanced Packaging: Remarkable Growth

According to a report released by consulting firm Yole Group in July last year, driven by trends in HPC and generative AI, the advanced packaging industry is expected to achieve a compound annual growth rate (CAGR) of 12.9% over the next six years. Specifically, the overall revenue of the industry is projected to grow from $39.2 billion in 2023 to $81.1 billion by 2029 (approximately 589.73 billion RMB).

Industry giants, including TSMC, Intel, Samsung, ASE, Amkor, and JCET, are heavily investing in high-end advanced packaging capacity, with an estimated investment of about $11.5 billion in their advanced packaging businesses in 2024.

The wave of artificial intelligence undoubtedly brings new strong momentum to the advanced packaging industry. The development of advanced packaging technology can also support the growth of various fields, including consumer electronics, high-performance computing, data storage, automotive electronics, and communications.

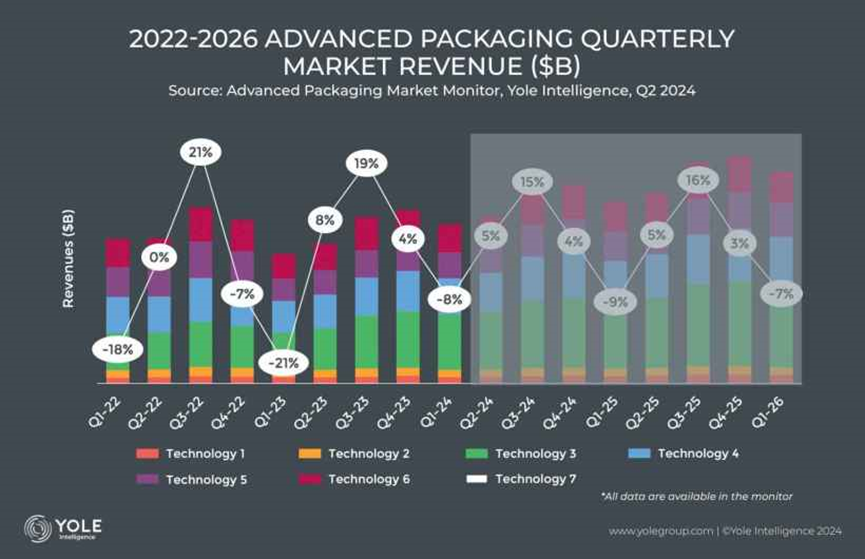

According to the company's statistics, the revenue from advanced packaging in the first quarter of 2024 reached $10.2 billion (approximately 74.17 billion RMB), showing an 8.1% decline quarter-on-quarter, primarily due to seasonal factors. However, this figure is still higher than the same period in 2023. In the second quarter of 2024, advanced packaging revenue is expected to rebound by 4.6%, reaching $10.7 billion (approximately 77.81 billion RMB).

Although the overall demand for advanced packaging is not particularly optimistic, this year is still expected to be a recovery year for the advanced packaging industry, with stronger performance trends anticipated in the second half of the year. In terms of capital expenditure, major participants in the advanced packaging field invested approximately $9.9 billion (approximately 71.99 billion RMB) in this area throughout 2023, a 21% decline compared to 2022. However, a 20% increase in investment is expected in 2024.

Post time: Jun-09-2025